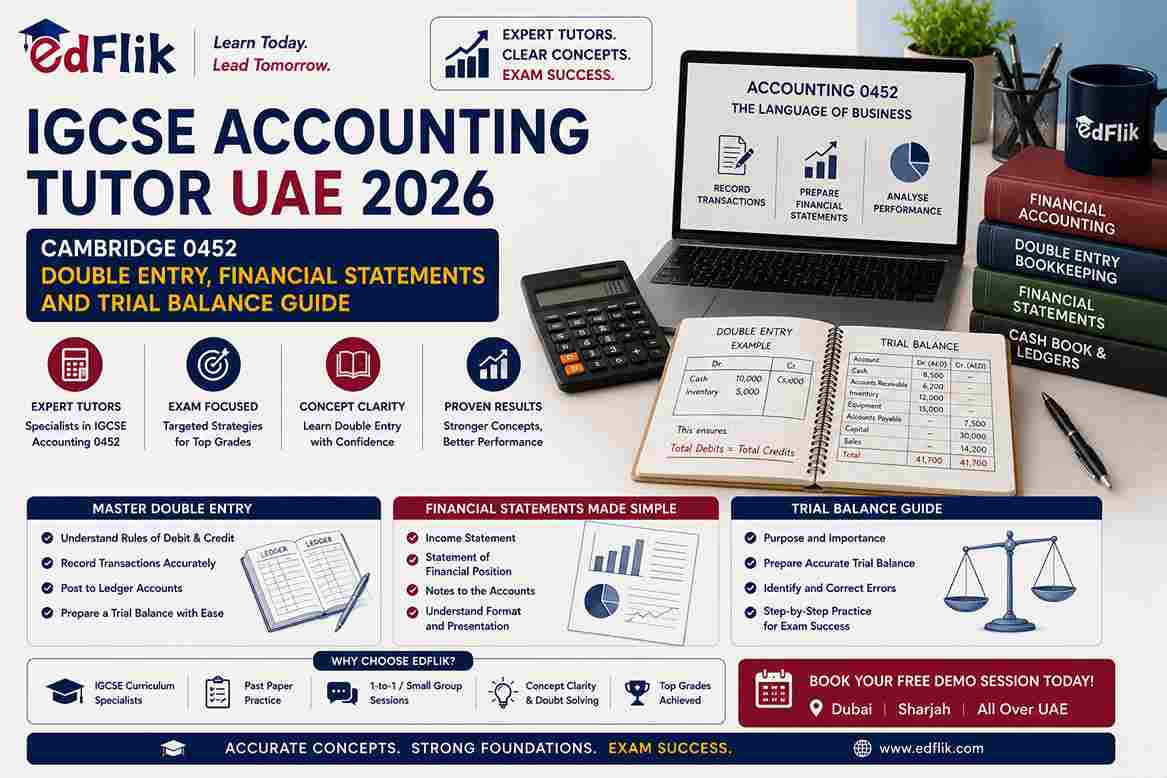

IGCSE Accounting Tutor UAE 2026 — Cambridge 0452 Double Entry, Financial Statements and Trial Balance Guide

IGCSE Accounting (Cambridge 0452) is one of the most rewarding commerce subjects UAE students can take — it builds a precise, systematic skill set that directly supports Business Studies, Economics, and any future career in finance. It is also one of the most method-dependent subjects: students who understand the underlying logic of double entry perform consistently well; students who try to memorise rules without the logic struggle to apply them in new situations. This guide covers the double entry system, ledger account format, trial balance, financial statements, and accounting ratios.

IGCSE Accounting Paper Structure — Cambridge 0452

|

Paper |

Content |

Duration |

% of Grade |

|

Paper 1 |

Multiple

choice — 30 questions covering all topic areas |

45 minutes |

30% |

|

Paper 2 |

Structured

questions — accounts preparation and analysis; some financial statement

preparation |

1 hour 45

minutes |

70% |

|

Cambridge

0452 Paper 2 (70% of grade) is where the grade boundary is determined. Most

Paper 2 questions require preparing ledger accounts, income statements, or

balance sheets accurately — mistakes in double entry format cost heavily. The

most effective exam preparation is repeated, timed practice of full financial

statement preparation from trial balance data. |

The Double Entry System — Understanding the Logic

The double entry system rests on one principle: every financial transaction has two aspects — a value received by one account (debit) and a value given by another account (credit). The total debits always equal the total credits.

|

Account Type |

Debit Rule |

Credit Rule |

Example |

|

Assets (cash,

receivables, inventory, equipment) |

Debit to

INCREASE |

Credit to

DECREASE |

Buying

equipment: Dr Equipment, Cr Cash |

|

Liabilities

(bank loan, trade payables) |

Debit to

DECREASE |

Credit to

INCREASE |

Taking a bank

loan: Dr Cash, Cr Bank Loan |

|

Capital

(owner's equity) |

Debit to

DECREASE |

Credit to

INCREASE |

Owner invests:

Dr Cash, Cr Capital |

|

Revenue

(sales, fees earned) |

Debit to

DECREASE |

Credit to

INCREASE |

Making a sale:

Dr Cash/Receivables, Cr Sales |

|

Expenses

(wages, rent, cost of sales) |

Debit to

INCREASE |

Credit to

DECREASE |

Paying wages:

Dr Wages Expense, Cr Cash |

The most common UAE student error: treating debit and credit as "good" and "bad." Debit and credit are neutral — they simply indicate which side of the T-account the entry belongs to. An asset increasing is a debit; an expense increasing is also a debit. Understanding why (both increase a debit-balance account type) is more reliable than memorising rules.

Ledger Accounts — T-Account Format

Every account in IGCSE Accounting uses the T-account format: Date | Details | Folio | Debit Amount on the left; Date | Details | Folio | Credit Amount on the right. The balance is found by totalling each side and carrying down the difference. Examiners specifically award marks for: correct account title, correct date format, correct counter-account name in the Details column (showing the double entry), and correct balance carried down.

The Trial Balance

The trial balance lists all account balances after posting all transactions. Debit balances include: assets, expenses, drawings. Credit balances include: liabilities, capital, revenue. If debits equal credits, the bookkeeping is internally consistent (though not necessarily correct — the trial balance does not detect all error types).

Errors the Trial Balance Does NOT Detect

• Error of omission — a transaction that was not recorded at all

• Error of commission — a transaction posted to the wrong account of the same type (e.g. posted to the wrong supplier account)

• Error of principle — a transaction posted to the wrong account type (e.g. a capital expense posted to the revenue expense account)

• Compensating errors — two errors that cancel each other out

Financial Statements — Income Statement and Balance Sheet

Income Statement Format

Revenue (Sales); minus Cost of Sales (Opening Inventory + Purchases + Carriage Inwards - Closing Inventory) = Gross Profit; minus Operating Expenses (wages, rent, depreciation, bad debts) = Operating Profit; plus/minus Non-operating items (interest received, interest paid) = Net Profit Before Tax.

Balance Sheet Format

Non-Current Assets (land, buildings, equipment — shown at cost minus accumulated depreciation = carrying amount); Current Assets (inventory, receivables, prepayments, cash — at current value); Total Assets; minus Current Liabilities (payables, accruals, bank overdraft); minus Non-Current Liabilities (long-term loans); equals Net Assets; equals Capital (Opening capital + net profit - drawings).

Accounting Ratios — Calculation and Interpretation

|

Ratio |

Formula |

What It

Measures |

Interpretation |

|

Gross Profit

Margin |

(Gross Profit

/ Revenue) x 100 |

Profitability

of trading activities |

Higher is

better; compare year-on-year and against industry benchmark |

|

Net Profit

Margin |

(Net Profit /

Revenue) x 100 |

Overall

profitability after expenses |

Lower than

GPM; the gap shows expense efficiency |

|

Return on

Capital Employed |

(Net Profit /

Capital Employed) x 100 |

Return on the

total investment in the business |

Should exceed

the cost of borrowing to justify the investment |

|

Current Ratio |

Current Assets

/ Current Liabilities |

Short-term

liquidity |

Typically

1.5:1 to 2:1 comfortable; below 1:1 is a concern |

|

Acid Test

Ratio |

(Current

Assets - Inventory) / Current Liabilities |

Quick

liquidity (excluding slow-to-sell inventory) |

1:1 is

typically adequate; below 0.75:1 signals liquidity risk |

|

Inventory

Turnover |

Cost of Sales

/ Average Inventory |

How many times

inventory is sold and replaced per year |

Higher = more

efficient; lower = risk of obsolete stock |

|

EdFlik IGCSE

Accounting tutors are Cambridge 0452 specialists. Sessions focus on double

entry logic, ledger account preparation, financial statement building, and

ratio interpretation. From AED 60 per session. Free diagnostic trial. Book at

www.edflik.com or WhatsApp +91 88788 96600. |

Frequently Asked Questions

Q: Is IGCSE Accounting hard?

Method-dependent rather than inherently hard. Students who understand the logic of why debits and credits work perform consistently well. Memorising rules without understanding the logic leads to difficulty when questions present new situations.

Q: What is double entry bookkeeping in IGCSE Accounting?

Every transaction has two entries: a debit in one account and an equal credit in another. Assets and expenses increase with a debit; liabilities, capital, and revenue increase with a credit.

Q: What is the trial balance in IGCSE Accounting?

A list of all account balances showing debits and credits. If total debits equal total credits, bookkeeping is internally consistent. A balanced trial balance does not guarantee all errors have been caught — errors of omission, commission, principle, and compensating errors are not detected.

Q: What financial statements are included in IGCSE Accounting?

Income Statement (gross profit, net profit), Balance Sheet (assets, liabilities, capital), and basic Cash Flow Statement. Students must prepare these from trial balance data and interpret them using accounting ratios.

Q: What accounting ratios are in IGCSE Accounting?

Profitability: Gross Profit Margin, Net Profit Margin, ROCE. Liquidity: Current Ratio, Acid Test Ratio. Efficiency: Inventory Turnover, Trade Receivables Days. Each requires both calculation and written interpretation.